FII DII Investing in a Shrimp Exporter Amid FTA Winds and Margin Pressures

1. Fundamental Analysis

Business Overview

- Apex Frozen Foods Ltd. is one of India’s leading shrimp processors and exporters, deriving 95%+ of its revenue from exports. Its main export markets are the US (now 45–50%, down from 60–65%), the EU (notably ~39% in Q4 FY25, up sharply), UK, and select Asian countries.

- Product focus: Whiteleg and black tiger shrimp—both raw and value-added (ready-to-eat, branded lines).

- Market Cap: ₹793Cr

- Current Price: ₹254

- ROCE: 2.46%

- ROE: 0.78%

- Dividend Yield: 0.8%

- Debt/Equity: ~0.22, indicating low leverage

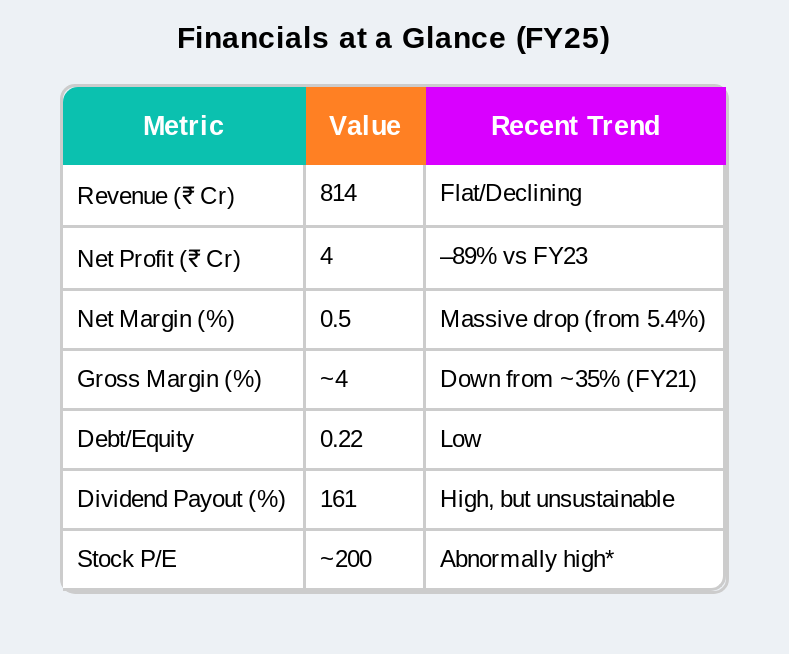

Financials at a Glance (FY25)

Table 1. Financials at Glance

Note :PE is high due to earnings drop. If earnings grow to the level of FY23 then PE can drastically reduce to 15-30.

Recent Management Insights

- Growing EU Focus: As per Q4 FY25 concall, EU (excluding UK) now forms ~36% of sales (up from 22% YoY), with total FY25 EU share at 39%. Management expects the UK’s share to cross 10% after full FTA/product approvals.

- US Market: Still critical but decline in share. US tariffs (including a fresh 10% in FY25) have added uncertainty. Management remains “cautiously optimistic” about US trade normalization and is increasingly diversifying.

Pros

- Debt has reduced considerably, lowering financial risk

- Maintains healthy dividend payout (recent payout: 161%)

Cons

- Sales growth is negative: -0.33% CAGR over 5 years.

- Profitability sharply declining: 73% fall in TTM profits.

- ROE and ROCE have fallen to record lows.

2. Financial Statement Analysis (FY25 Snapshot)

| Metric | Mar 2023 | Mar 2024 | Mar 2025 |

| Revenue (₹ Cr) | 1,070 | 804 | 814 |

| Operating Profit (₹ Cr) | 83 | 41 | 25 |

| OPM % | 8% | 5% | 3% |

| Net Profit (₹ Cr) | 36 | 15 | 4 |

| EPS (₹) | 11.48 | 4.67 | 1.24 |

| Debt/Equity | 0.18 | 0.22 | 0.22 |

| Dividend Payout (%) | 22 | 54 | 161 |

| ROE (%) | 3.7 | 1.0 | 0.78 |

Table 2: FSA

Trend: Revenues are flat or declining; sharp drop in margins and profits since FY23.

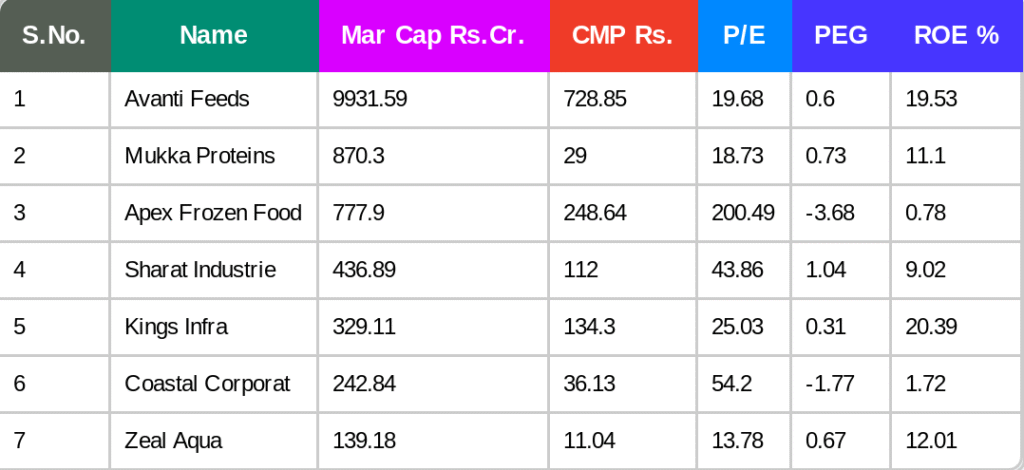

3. Relative Valuation with Top 5 Indian Competitors

Table 3: Relative Valuation

Valuation Insight: Apex’s P/E remains abnormally high due to profit collapse, as highlighted by management: “Profitability has sharply declined… margins have compressed due to both cost and demand issues” (Q4 & Q3 FY25 concall’s).

4. Why Margins & Profits Collapsed

- Raw Material Costs: “Persistent elevation in farm-gate shrimp prices due to supply shortages” — Q2 & Q3 FY25 concalls.

- Stagnant Prices: “Selling prices could not rise in sync with global inputs due to intense competition from SE Asia” — management, multiple concalls.

- Tariffs: “The US reciprocal 10% tariff has created a trade war-like scenario. Earlier countervailing duties went up to 26%.” (Q4 FY25).

- Overheads: “Shipping and logistics costs…remained elevated through FY25, hitting margins and bottom-line.”

- Low Utilization: “Plant utilization for Q4 was only ~20%, averaging 30% for the full year – much below our potential,” management highlighted in Q4 FY25.

5. Is There a Path to Recovery?

Positive Developments:

- EU Expansion: “EU (excluding UK) grew to 36% of quarterly sales in Q4, helped by rapid uptake and market share gains.”

- RTE Product Regulatory Approvals: “EU approval for our ready-to-eat (RTE) product line is a key near-term trigger. If approved, we expect to ramp up EU RTE sales by 2,500MT in year one,” management stated (Q4 & Q3 FY25).

- UK FTA Impact: “After full approvals, UK revenue share expected to rise >10%. FTA has eliminated marine export tariffs, boosting competitiveness.”

- Margin Signs: “Starting Q4 FY25, gross margin has rebounded to ~30% (up 500bps QoQ),” CEO in June 2025 call.

Caution/Headwinds:

- US Tariff Uncertainty: “US trade/tariff scenario still risky. We remain dependent on bilateral resolution for full recovery.”

- Continued Margin Squeeze: “Despite improvement, operating margins remain well below pre-FY22 levels.

6. Technical & Relative Valuation

- Short-Term Price Action: Recently trending up, above all major moving averages, with bullish momentum in the short run. Still, volatility is high and medium/long-term trends remain weak.

- Relative Value: Apex’s P/E (~200) towers over peers like Avanti Feeds (12–15) because of minuscule earnings. Unless profitability rebounds, valuation is unattractive.

7. Key Opportunities and Risks Table

| Opportunity | Risk |

| FTA-led UK/EU market growth | US tariff volatility |

| RTE & value-added product approvals | Flat/loss-making core operations |

| National export incentives | Input cost inflation |

| Operating leverage from volume | Aggressive SE Asia price competition |

| Brand/Credentials (ISO, BAP, BRC) | Dependence on few large buyers |

Table 4: Key Oppurtunities

8. Should You Invest Now?

Hold/Buy Rationale:

- Margins may have bottomed; any cost relief or demand uptick could sharply boost profits due to high operational leverage (“We expect meaningful margin and profit inflection once RTE is cleared for exports,” Q4 FY25).

- Recent FTAs and value-added drive offer a turnaround case, if management executes successfully.

- Short-term price action positive; tactical opportunities for traders.

Wait/Avoid Rationale:

- Persistent cost/demand/margin pressure can quickly halt or reverse rallies.

- Historic margin compression and flat sales, with institutional investor reticence—”Show me” story.

- Unless margin recovery visible and higher-value segments realized, fundamental upside remains speculative.

Management Guidance:

“We believe the business has turned the corner in Q4 FY25, but sustained improvement depends on external approvals and trade policy clarity. Capex will remain minimal until volume certainty returns.” (Management, Q4 & Q3 FY25)

9. Concall Highlights

Quarterly Growth & Geographies:

- Q3–Q4 FY25: Revenue improved 22% YoY (Q4), with EU now at 36–39% of quarterly sales, US declining to ~45%.

- Management expects the UK to cross 10% of revenue as FTA benefits and approvals flow in.

- Q2–Q3 FY25: Sequential and YoY revenue growth (Q3 up 16% QoQ, 56% YoY).

US Tariffs:

- 10% reciprocal tariff in force as of FY25, after earlier duties that reached 26%, causing significant margin compression.

Margin Outlook:

- Gross margin rebounded to ~30% in Q4 FY25; management expects further improvement once RTE business in EU is approved and demand in key markets normalizes.

Detailed Causes of Margin Compression:

- High shrimp procurement (raw material) prices.

- Elevated logistics/freight/energy costs.

- Low plant utilization (20–30% only).

- Tariff pressure in main markets (US).

- Order volatility and lumpy demand from overseas buyers.

Management’s Estimation for Margin Recovery:

- Margin normalization and earnings rebound could come during FY26, “once global market volatility abates and key product approvals in the EU/UK are secured.”

10. Bottom Line

Apex Frozen Foods is attempting a turnaround with renewed EU/UK focus, regulatory triggers (RTE approvals), and FTA-driven opportunities. However, recovery depends heavily on external market, regulatory, and cost normalization. Investors should actively track quarterly margin rebound and volume traction, especially from the EU/UK. True risk/reward will emerge only with visible, sustained improvement in margins and regulatory green lights.

Always consult a financial advisor before making investment decisions. For serious research, review the latest concall transcripts alongside fundamentals.

References: Screener.in, Moneycontrol, company annual reports and official concall transcripts (Q2 FY24 to Q4 FY25).