Sector Context

Small finance banks (SFBs) are critical drivers of financial inclusion in India, focusing on underserved and unbanked populations, especially in rural and semi-urban areas. Among them, AU Small Finance Bank stands out as the sector leader, with a robust franchise, strong growth, and consistent financial performance. To gauge its relative strength, we compare AU SFB with Ujjivan SFB, Utkarsh SFB, and two larger private sector banks—IndusInd Bank and IDFC First Bank—across five key metrics: Price to Book (P/B) ratio, Return on Equity (ROE), Net Interest Margin (NIM), Net NPA, and Gross NPA

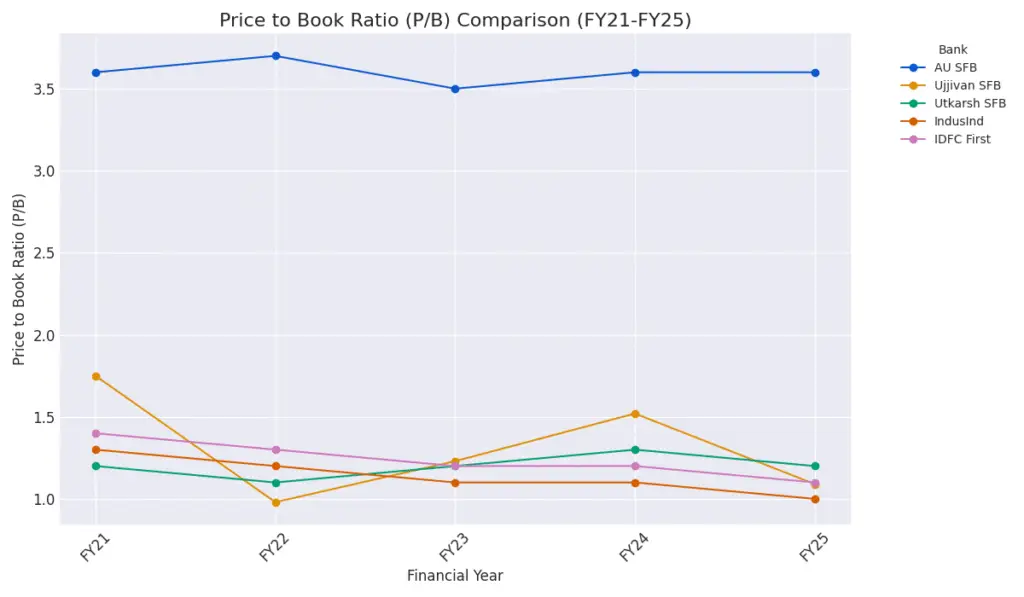

Valuation: Price to Book (P/B) Ratio

AU SFB commands a premium valuation, with its P/B ratio consistently in the 3.5–3.7x range over the last five years. This reflects strong investor confidence, underpinned by stable profitability and asset quality. Ujjivan SFB’s P/B has declined from 1.75x in FY21 to 1.09x in FY25, mirroring past asset quality concerns and volatility. Utkarsh SFB has maintained a steady but modest P/B of 1.1–1.3x, reflecting its smaller scale and recent asset quality stress.

By comparison, IndusInd Bank and IDFC First Bank trade at lower P/B multiples (typically 1.0–1.4x), reflecting their larger, more diversified franchises but also the market’s more cautious view of their growth and asset quality profiles.

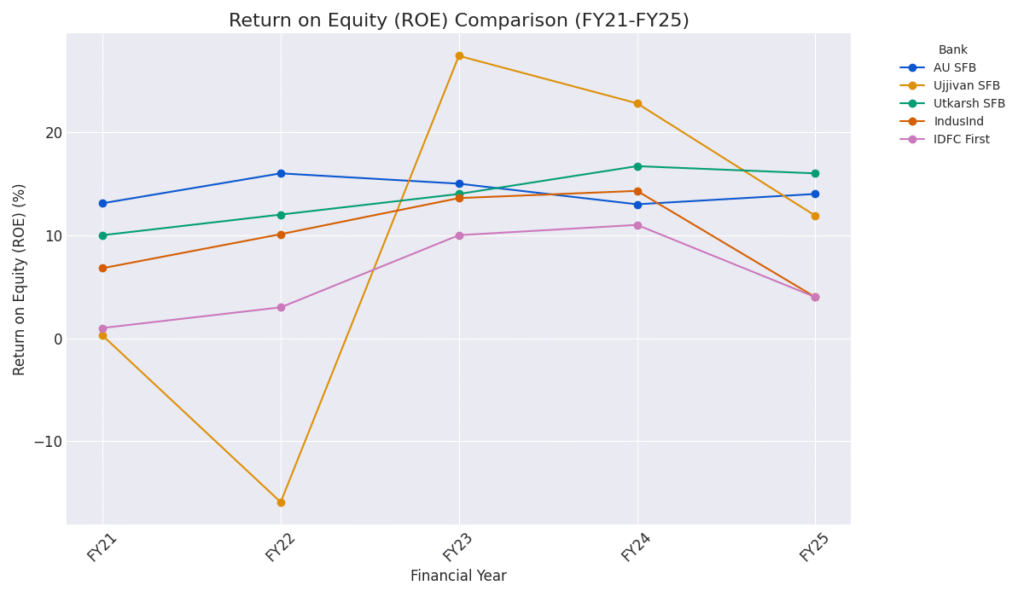

Profitability: Return on Equity (ROE)

AU SFB has delivered a steady ROE of 13–16%, indicating robust and predictable earnings. Ujjivan SFB saw sharp swings—plummeting to –15.9% in FY22 (due to pandemic-related stress), rebounding to 27.4% in FY23, and stabilizing at 11.9% in FY25. Utkarsh SFB has shown a healthy uptrend, with ROE rising from 10% in FY21 to 16% in FY25, thanks to improving earnings efficiency.

Among the larger peers, IndusInd Bank’s ROE peaked at 14.3% in FY24 but dropped to 4% in FY25, likely due to provisioning or margin pressures. IDFC First Bank has improved from 1% to 4% over five years, but still trails the SFBs in profitability.

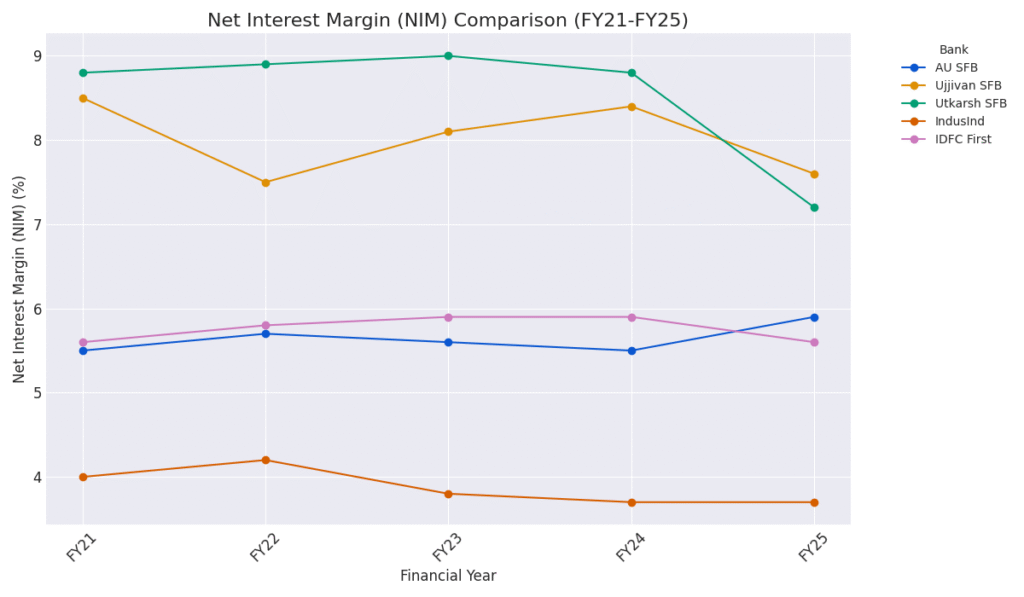

Margins: Net Interest Margin (NIM)

AU SFB maintains a stable NIM of 5.5–5.9%, supported by its retail-heavy loan book and granular deposit base. Ujjivan SFB and Utkarsh SFB report even higher NIMs (7–9%), reflecting their focus on high-yield microfinance and MSME lending. However, Utkarsh SFB saw margin compression to 7.2% in FY25, likely due to increased funding costs and asset quality stress.

For context, IndusInd Bank and IDFC First Bank operate with lower NIMs (3.7–5.9%), typical for larger banks with more diversified portfolios and lower-risk lending.

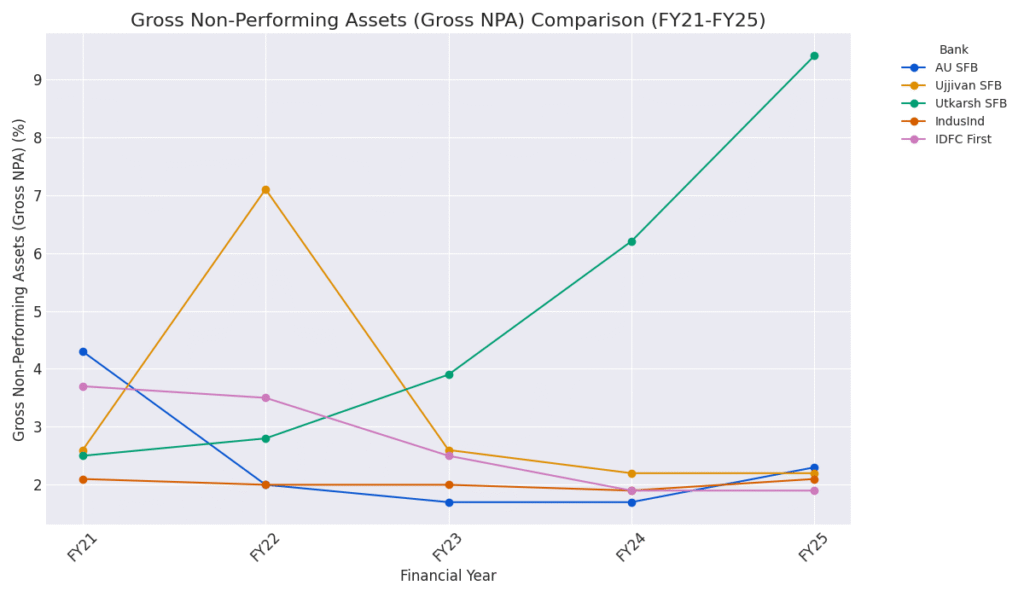

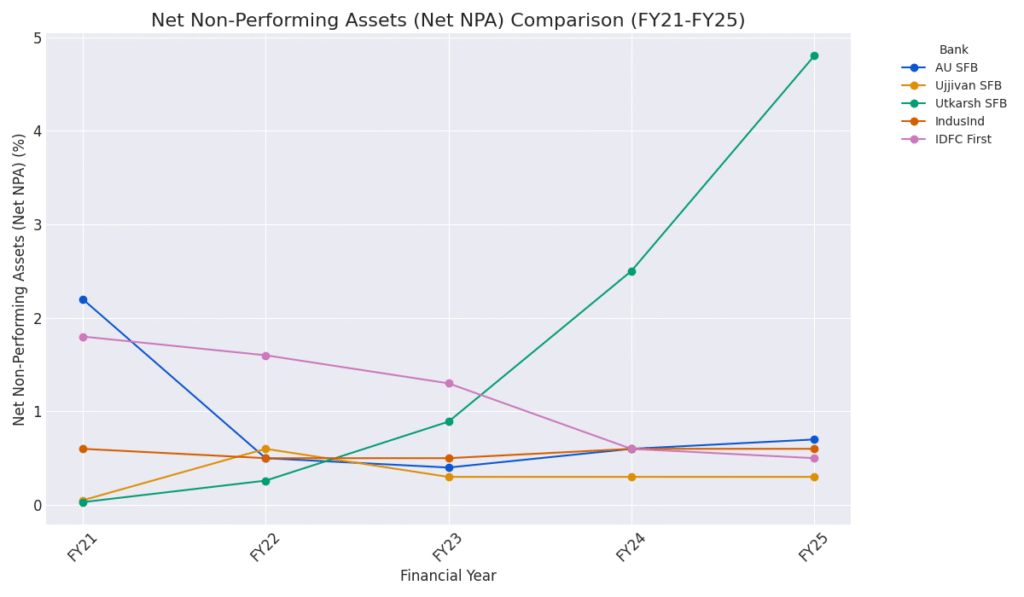

Asset Quality: Net NPA & Gross NPA

AU SFB has demonstrated significant improvement in asset quality: Net NPA fell from 2.2% in FY21 to 0.7% in FY25, and Gross NPA from 4.3% to 2.3%. Ujjivan SFB has kept Net NPA low and stable (0.3–0.6%), with Gross NPA reducing from a peak of 7.1% in FY22 to 2.2% in FY25, reflecting strong risk management. In contrast, Utkarsh SFB’s asset quality has deteriorated sharply: Net NPA jumped from 0.03% to 4.8%, and Gross NPA surged from 2.5% to 9.4%—a red flag for future profitability and valuation.IndusInd Bank and IDFC First Bank have maintained relatively stable and low NPAs, with Net NPA around 0.5–0.6% and Gross NPA around 1.9–2.1% in FY25, reflecting their larger and more diversified loan books.

Insights & Takeaways

-

- AU SFB’s premium valuation is justified by its consistent ROE, stable NIM, and improving asset quality, positioning it as the sector benchmark.

-

- Ujjivan SFB has emerged as a credible second-tier player, having overcome past volatility with a cleaner balance sheet and improving profitability.

-

- Utkarsh SFB enjoys high margins but faces mounting asset quality challenges, which could weigh on future growth and investor sentiment.

-

- IndusInd Bank and IDFC First Bank offer stability and scale, but their profitability and valuation multiples are lower than the best-performing SFBs, reflecting the trade-off between growth and risk in the sector.

Conclusion

AU Small Finance Bank remains the clear leader among SFBs, combining growth, profitability, and asset quality. Its premium valuation is supported by fundamentals and market confidence. Ujjivan SFB is on a strong recovery path, while Utkarsh SFB must urgently address asset quality. For investors, AU SFB offers a compelling blend of stability and upside, even as larger banks like IndusInd and IDFC First provide diversification and scale.

The future of India’s small finance banks is promising, with financial inclusion and digital banking driving long-term growth. AU SFB’s leadership in this space makes it a top pick for fundamental investors in the sector.

Sources: Screener.in, Moneycontrol, Share.Market, FinShiksha, Financial Express, company filings, and sector reports.