1. Company Profile & Business Overview

- Avanti Feeds Ltd (AFL): India’s largest shrimp feed producer and a significant exporter of processed shrimp, serving both domestic shrimp farmers and global buyers (notably USA, EU, Japan, Middle East).

- Product Mix:

- Shrimp Feed: ~78–80% of overall revenue (core profit driver; dominant market share).

- Shrimp Processing & Exports: ~20–22% revenue, growing via value-added and RTE (Ready-to-Eat) products.

- Pet Food: Newly launched (2025), negligible contribution.

- Geographical Split:

- Domestic (mainly feed): ~78–80% revenue.

- Exports (mainly processed shrimp): ~20–22% revenue, with ongoing diversification to reduce US dependence.

- For more detailed analysis of Seafood Industry in india. Read this blog

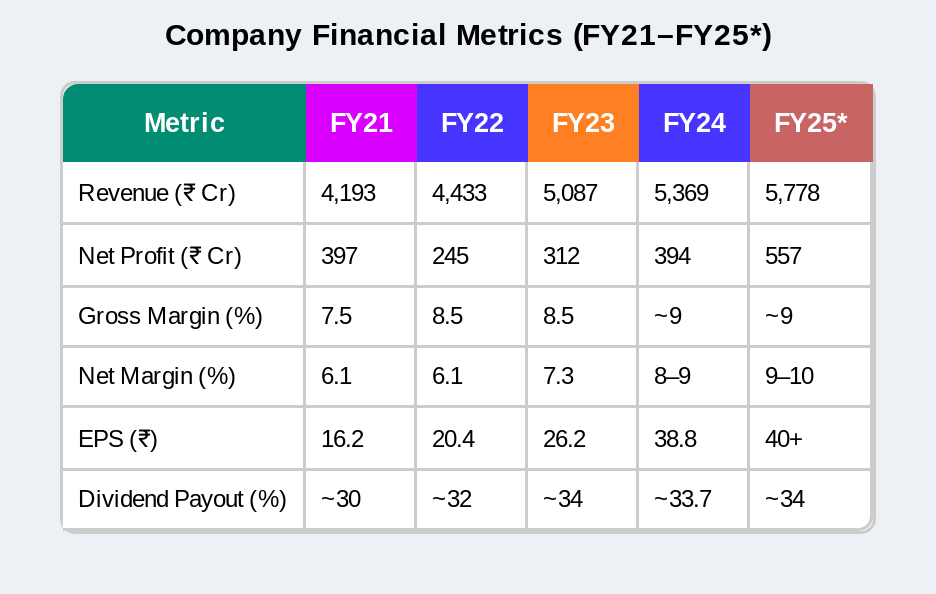

2. Key Financials & Growth Trends

Last 5 years

Tab 1. Company Financial metrics from FY21 to FY25

- Growth: Five-year CAGR (FY21–25): Revenue ~8%; consistent profit expansion.

- Margins: Improved steadily owing to scale, cost controls, and product/value-add mix.

- Balance Sheet: Debt-free, high cash, robust free cash flow.

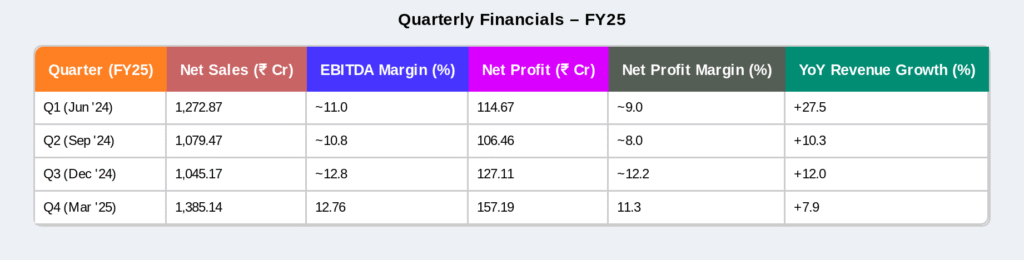

LAST 4 QUARTERS

Tab 2. Quarterly Financials

Commentary:

- Revenue Growth: Every quarter YoY growth was positive, with Q4 up 7.9% and the full year showing mid-single-digit volume-led expansion.

- Profit Margins: Gross margin and EBITDA margin expanded sharply in Q3 and Q4 FY25, reflecting improved cost management and product mix.

- Profit Growth: Net profit for Q4 FY25 grew 39.6% YoY, a substantial leap woven from both higher volumes and margin expansions. Yearly profit growth was robust following steady demand and optimized costs.

- Cash Conversion: As seen in previous years, the profit/CFO ratio remains healthy overall, indicating efficient conversion of profits to operating cash.

3. Detailed Revenue & Product Split (FY25)

- Shrimp Feed (Domestic): ~78–80% of revenue; market leader; resilience during global volatility due to local demand.

- Processed Shrimp (Export): ~20–22%; focus on value-added/RTE. Exports by region: US (largest), followed by EU, Japan, Middle East.

- Pet Food: Negligible as of FY25.

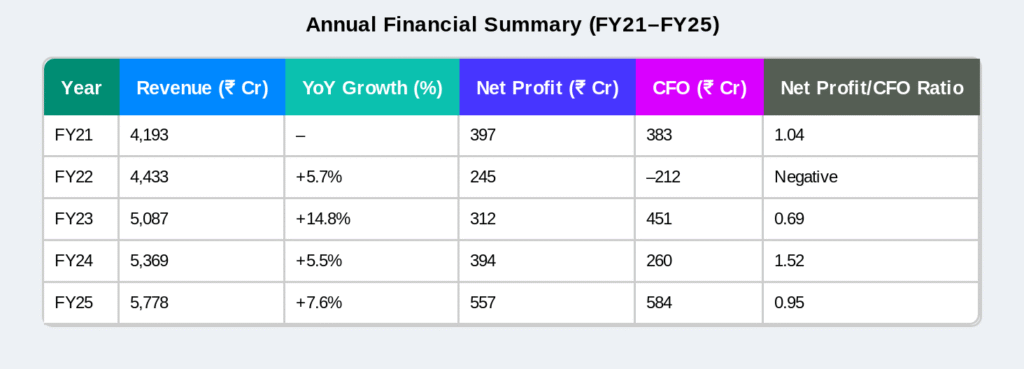

4. Sales Growth, Profitability, and Cash Flow (Last 5 Years)

Tab 3. Annual Financial summary

CEO Commentary: Consistent profit-to-cash conversion, except FY22 when working capital outflow distorted CFO.

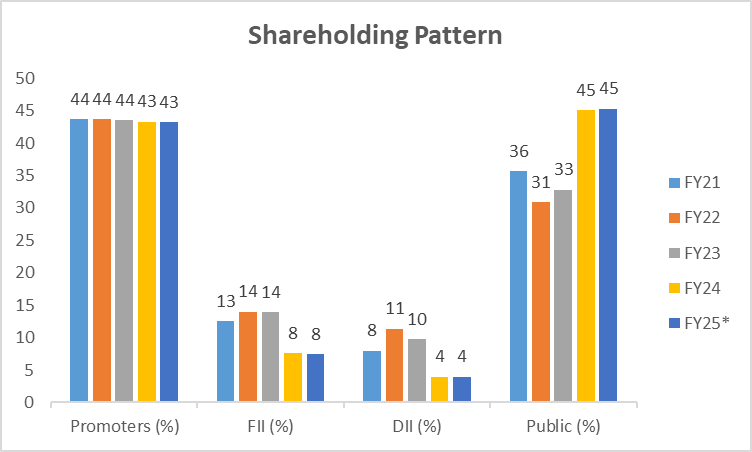

5. Shareholding Pattern: Promoter, FII, DII (Past 5 Years)

chart 1. Shareholding pattern

Institutional Trend: FII/DII increased till FY23, then declined sharply in FY24–25 as retail participation rose.

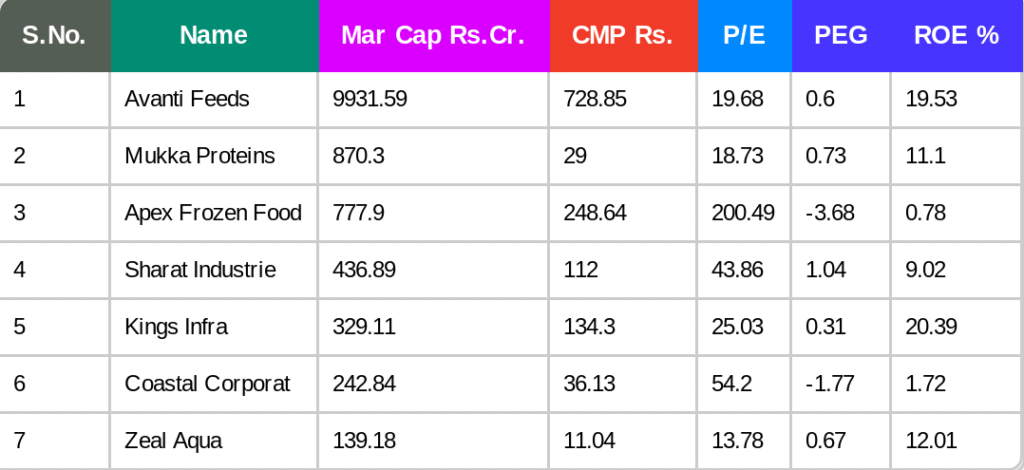

6. Relative Valuation Vs. Peers (July 2025)

Tab 4. Relative valuation

Interpretation: Avanti’s returns, scale, and margin profile justify a premium over sector peers.

7. Key Qualitative & Management Insights

- Management Quality: Highly regarded for prudence, low leverage, and capital discipline. Regular disclosures, transparent conductor of concalls, and judicious expansion (focus on automation/value-add, not reckless capex). Board led by promoter Alluri Indra Kumar.

- Operational Efficiency: Consistently high plant utilization (feed >80%, processing >65%). Technology upgrades and cost control yield industry-leading margins.

- Risk Management: Quick market/geography/product diversification. Maintains net cash, avoids speculative expansions.

8. Concall & Annual Report Highlights (FY24–Q1 FY26)

- Geographic Diversification: Sustained US leadership, accelerated penetration in EU/Japan/Middle East.

- Product Development: RTE/Value-Added plant scaled in FY24, growing >8% of exports already; target 15%+ in FY26.

- Profitability Drivers: Resilient procurement, pricing power in feed, and greater value addition in processing.

- Capex: Focused, mostly maintenance and value-addition—not expansion driven.

- Q1 FY26: Management expects further sales/profit growth as global shrimp demand normalizes.

9. Opportunities & Risks

| Opportunity | Risk |

| RTE & value-added product expansion | Global shrimp price/cycle volatility |

| Export market rebound | Farmer distress, input price swings |

| Strong domestic/feed business | Tariffs, USD/INR volatility |

| Cost/tech leadership | SE Asia competition |

| Industry reputation, balance sheet | Overreliance on shrimp cycle |

10. Credit Ratings

- Long-term: IND AA- (Stable)

- Short-term: IND A1+

- Takeaway: Ratings confirm robust liquidity, prudent management, and strong business position.

11. Bottom Line

- Sector Leader: Avanti Feeds is India’s most diversified, cash-rich, and efficiently run aquaculture and feed business, with a margin profile and risk management approach that set it apart from smaller sector players.

- Outlook: Execution on scaling RTE/value addition and maintaining cost/market discipline are key. Growth visible but not risk-free given industry cyclicality.

- Investor Note: Rapid sales/profit recovery, robust cash flow (except FY22 working capital blip), and balance sheet strength support long-term conviction, even as some institutional money has reduced post-pandemic.

12. My Take: What Investors Should Really Watch

In my view, Avanti Feeds is a fundamentally solid leader with a sound balance sheet, steady execution, and the right strategic pivots (notably, RTE/value-added expansion and the strong global partnership with Thai Union). However, investors should keep a close watch on two key macro drivers:

- US Tariffs on Indian Shrimp: Any escalation or resolution here can swing fortunes for Indian shrimp exporters, including Avanti. Uncertainty persists in 2025; future trade agreements or tariff rollbacks could unlock meaningful export growth and margin release.

- Performance of Global Shrimp Sellers: Track the health and pricing power of leading international shrimp companies (including those in the US, Thailand, Vietnam). Their realization and inventory trends will signal demand-supply cycles and pricing pressure points for Avanti.

On Valuation and Price

- The stock looks increasingly attractive in the ₹600–650 range—at this zone, the downside appears limited given Avanti’s margin profile, cash-rich status, and sector leadership. Upside exists, but is likely to be steady and moderate—not a multibagger scenario, at least in the near future.

- Over the past five years, the stock has mostly moved sideways, reflecting both sector cyclicality and lack of major re-rating triggers.

- If trade deals and global market access improve, Avanti stands as a quality long-term holding, especially for those seeking low-risk, moderate-compounder stocks with visible cash flows and disciplined management.

Disclaimer: This analysis is for educational purposes only and does not constitute a buy or sell recommendation. Please consult your financial advisor before making any investment decisions.

Always consult your financial advisor for investment suitability. Rely on the latest annual reports and investor calls for granular detail or major developments.

Data as of 26th July 2025; sourced from company reports, conference calls, Moneycontrol, Screener.in, and credit agency ratings.